Note to reader: As I have been saying for a long time now, I estimate the neutral Fed funds rate to be exactly what it is right now, 4.25%. There is a growing consensus that the FED may be done cutting overnight rates, since the employment and GDP data continue to remain robust, while the elevated inflation growth remains sticky.

I also note that the blame for these higher worldwide bond yields are being pinned on the incoming Trump regime. Although this is not justified, this all points to the higher costs of money and only those who have positioned themselves to benefit from higher inflation (e.g. underlevered landlords that can generate higher rent rolls and publicly traded firms and other businesses with inelastic demand) should actually benefit.

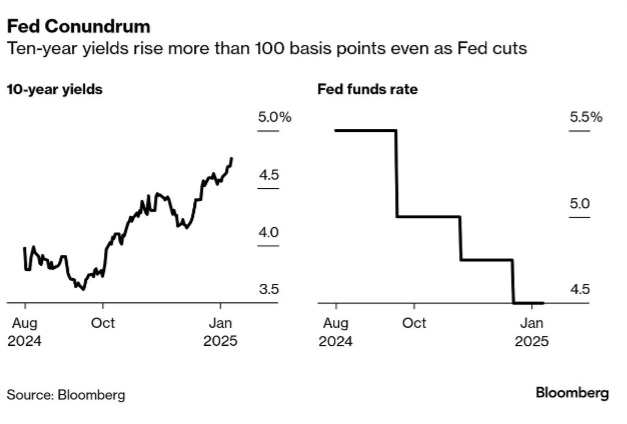

This blog has been noting the upward shift in the longer end of the yield curve, since the FED began cutting rates as an important dynamic to watch. However, it has not yet translated into lower stock prices. Since I have estimated that the neutral Fed funds rate was higher than others on the street estimated, I suspect stock prices will eventually adjust to a 10-year Treasury yield of 5.0 to 5.5%.

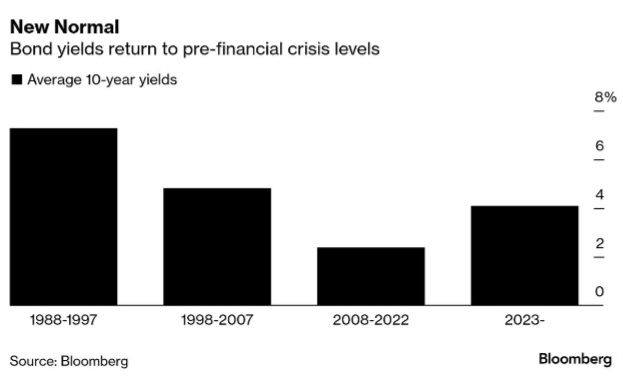

I suspect that real sovereign bond yields continue to grind higher, because there is a growing loss of confidence in the nation-state governments to control their ballooning fiscal deficits as well as the inability of the central banks to facilitate this outcome without generating higher trend inflation. In a world of global quantitative easing, these circumstances are without precedent.

If what I think will happen during Trump’s presidency does happen and the 10-year Treasury yield crosses 6%, circumstances in the asset markets could change quite markedly. It’s still not too late for investors to lock in 7% mortgages. I just raised the rents for several of my longer-term tenants by at least 5%. The world will adjust.

______________________

The Surging Cost of Money

From Bloomberg:

If strategists at Bank of America are correct, the US bond market is now in the sixth year of the third great bear market since 1790.

Few investors would beg to differ after a week in which US Treasury yields soared, propelling the rate on the 10-year note to the brink of the 5% barrier rarely seen since the financial crisis of 2008.

Other nations are experiencing a similar exodus from debt. The yield on 30-year UK gilts last week touched the highest since 1998, forcing the new Labour government to start seeking money-saving measures, and UK assets are weak again today.

The message from many in markets, and Bloomberg’s latest Big Take, is to get used to it: The price of money will be permanently higher as risks to the supposedly safest of assets mount.

Friday’s blowout jobs report shows the economy continues to power ahead, leaving Bank of America among those on Wall Street now betting the Federal Reserve won’t cut interest rates in 2025. Goldman sees two reductions, down from three previously.

With data this week set to show inflation is staying sticky (see our week ahead below), central bankers are already signaling they’re on hold.

And we are now a week away from the second Trump presidency which lands with promises of lower taxes and higher tariffs. That’s a recipe, in the opinion of many, for faster inflation and greater debt. A fight also looms over lifting the federal debt limit.

Put it all together and it’s no wonder the so-called term premium on 10-year notes — the extra yield investors demand to accept the risk of taking on longer-term debt — is now at a decade high.

The result is BlackRock, T. Rowe Price and Bianco Research are among those penciling in 5% as a reasonable target for yields amid expectations investors will demand juicier rates to keep buying longer-dated Treasuries.

That has implications for other markets, with historians noting the multiple times that higher borrowing costs have accompanied market and economic meltdowns.

Stock investors are already nervous the higher yields could bring an end to the tech-led bull run. The spillover in stocks was already apparent Friday as the S&P 500 fell 1.5%.

“There is a tantrum-esque type of environment here and it’s global,” said Gregory Peters, who helps oversee about $800 billion as co-chief investment officer at PGIM Fixed Income.